Poor credit scores are discouraging 15.6 million Brits from buying homes, getting married and changing careers, according to new research.

A survey commissioned by fintech firm Tymit reveals that worries about credit scores have delayed life milestones for nearly a third (29%) of Brits.

More than one in five (22%) have delayed buying a home due to their poor credit records, with damaged credit files reducing eligibility for mortgages.

Chequered financial pasts can also disqualify consumers from car finance products. 20% report that they’ve been unable to purchase a vehicle due to their credit scores.

Other dreams deferred include renovating a home (14%) and purchasing big-ticket items like digital devices (13%).

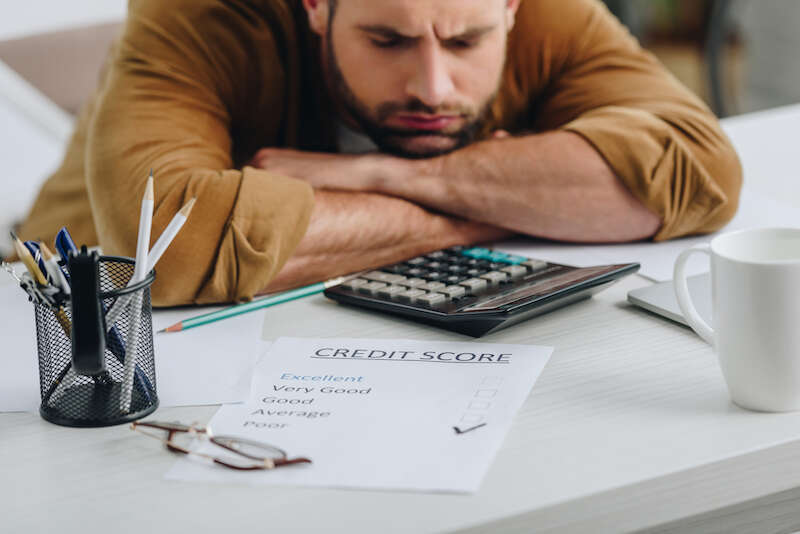

With credit files thwarting so many ambitions, it’s unsurprising that 38% of Brits who know their credit score report negative feelings about it. In fact, a quarter of consumers aware of their scores report that they negatively impact their mental health or leave them feeling “trapped.” Just half of consumers who know their scores are satisfied with them.

However, there are many misconceptions about credit scores—somewhat predictably given that nearly half (49%) of Brits don’t know their own.

28% don’t know how frequently lenders and retailers check their credit scores, and a similar percentage (23%) don’t know how credit scores are calculated.

This ignorance can push people into the red and damage their scores. For example, half of survey respondents don’t know that having no credit history at all can negatively impact their credit scores. Young consumers are advised to take out credit cards and clear the balance monthly to build positive credit history. Providers offer special credit building cards for this purpose.

Additionally, more than half (52%) of consumers don’t know that buy now pay later (BNPL) schemes can damage their credit scores if they miss payments. These services, from providers like Klarna and Clearpay, will face oversight from the Financial Conduct Authority (FCA) for the first time from next year, the government hoping regulation prevents people from unknowingly amassing debt using the payment plans pitched to them at online checkouts.

Conversely, many are unaware that the services for which they’re already paying can rehabilitate their scores. These include utility bills (energy and water) and Netflix and Spotify subscriptions—the top three things consumers don’t know can impact their credit rating.

Tymit is calling for better education of consumers about credit scores. Martin Magnone, founder and chief executive of the startup, said: “Your credit rating shouldn’t cost you your ambitions, but the reality is that hopes and dreams have been stalled for over 15 million of us. The misinformation around what our credit scores actually are, their function, and how they are calculated is only compounding the problem—it has to change.”

Tymit is a credit card that lets you spread the cost of everyday spending across weeks and months. Unlike traditional credit cards, interest is calculated from and applied to individual instalment plans rather than the whole balance. Ironically, it’s one of the BNPL schemes that many don’t know can affect their credit scores if they don’t keep up with payments.