Is comprehensive car insurance more expensive than other types of cover?

Not always. Because a comprehensive policy covers for more eventualities, you'd expect them to always be more expensive when all other factors are the same. However, in some cases insurers take into account the fact that high risk drivers are more likely to take out less comprehensive policies, so it's possible for a fully comprehensive policy to be less expensive than a third party policy.

This means that in high-risk categories, such as young drivers, fully comprehensive policies can sometimes be found at cheaper rates.

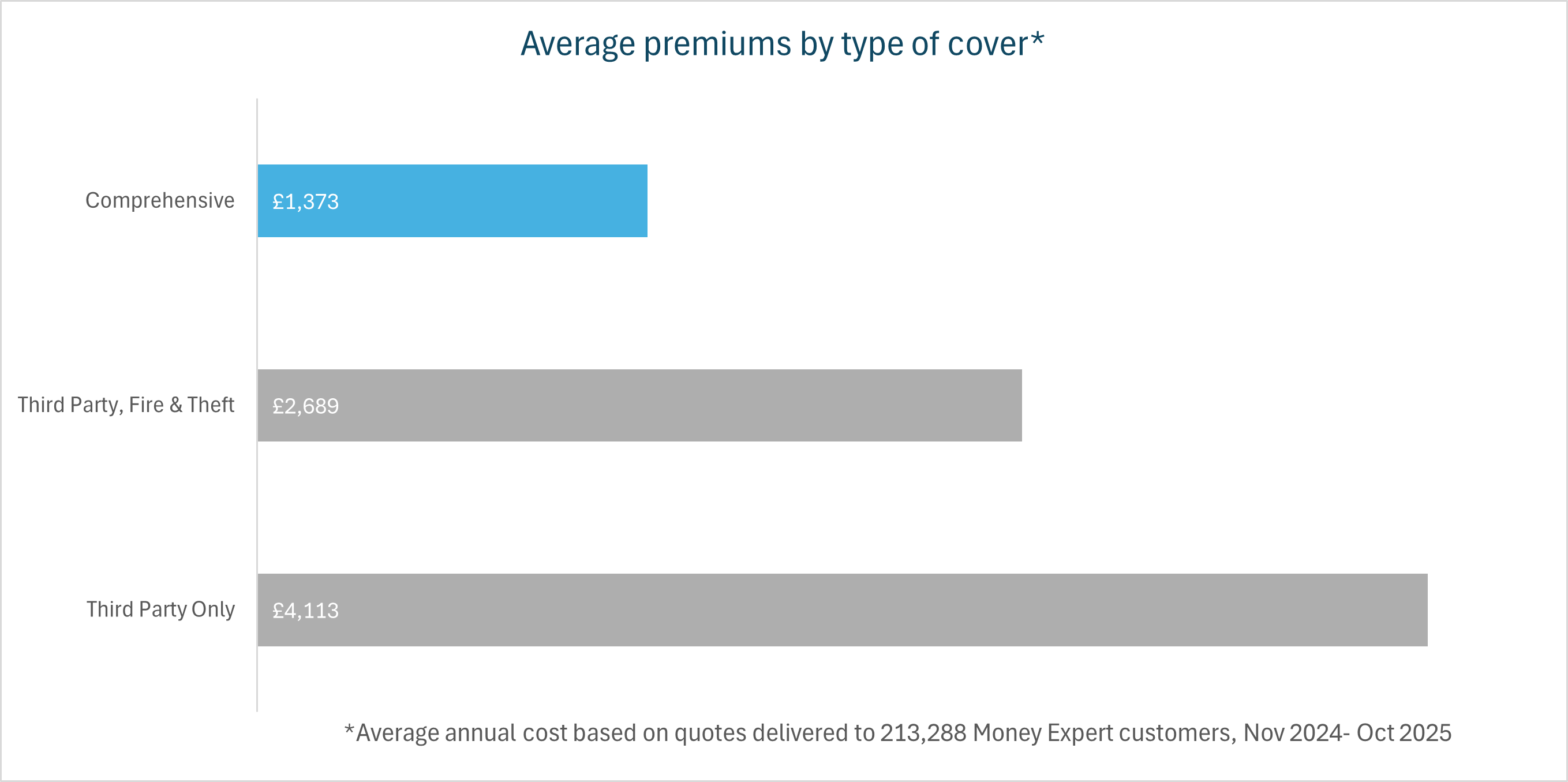

In fact, we found that customers looking for fully comprehensive cover were offered cheaper annual premiums than any others:

Fully comprehensive: £1,373

Fully comprehensive: £1,373

Third party, fire and theft: £2,689

Third party-only: £4,113