22

February 2024

Premiums hikes makes car insurance unaffordable for UK drivers

The average cost of car insurance has gone up a staggering 67% over the last 12 months according to the latest Consumer Intelligence data. This is down to inflation – many car insurance providers are finding replacement vehicles and repairs more expensive – coupled with an increase in claims. These extra costs are being passed onto consumers in the form of price increases.

Climate change is also having an impact. A rise in extreme weather events, like flooding and damage to homes from storms, can increase accidents and insurance claims, as well as damage to vehicles. As providers pay out more for claims relating to these events, car insurance premiums have risen in response.

Insurance fraud is another major contributor to the increase in car insurance premiums. Data published in August 2023 by the Association of British Insurers (ABI) showed around 42,500 motor scams were uncovered last year, which represented nearly two-thirds (59%) of total insurance claims fraud. To combat fraudulent claims, insurance providers have invested in anti-fraud measures and passed these additional costs on to policyholders.

Key anti-fraud measures include removing the right to general damages for soft tissue injuries to combat fraudulent whiplash claims and encouraging greater use of insurance data sharing and collaboration between regulatory bodies and the insurance sector. The upper limit for small claims courts for personal injury claims has also increased from £1,000 to £5,000.

We commissioned a survey to ask for your views on car insurance in the UK and the affordability annual policies following sharp increases in costs over the last few years. We also wanted to find out how these increases have impacted your spending, as well as any changes you may be considering to keep your car insurance premiums down.

Key findings

-

50% of those surveyed revealed that their annual car insurance had increased by up to £100

-

Nearly half (49%) said that further increases would result in them struggling financially to meet their car insurance payments

-

Only a quarter (25%) can afford their car insurance payments without making any changes such as downsizing their vehicle or cutting non-essential spending

-

One in five are considering downsizing their vehicle to afford rising costs

-

Over a third (35%) will have to pay their insurance in monthly instalments to make payments more manageable, despite this option being more expensive long-term

-

78% use a price comparison website like ours to find new deals

-

34% feel that there is no justification for the price increases

-

Over half (54%) say they tend to switch to different companies depending on who provides the most competitive price

-

Only one in 10 drivers have seen a reduction in their car insurance premiums in the last six months

Car insurance insights: How affordable is it for UK drivers?

Asking those surveyed to think about recent price rises, we wanted to know how affordable their car insurance was compared with previous years. We also wanted to know how concerned motorists were about the future affordability of car insurance premiums, if costs continue to rise.

When asked how much their latest car insurance premiums were, nearly half (46%) revealed that their current car insurance costs were between £251 to £500, while a quarter (25%) said that the latest car insurance costs were between £501 and £800.

Nearly half (45%) of drivers said that their previous car insurance costs were between £251 to £500, while 21% had said that car insurance had cost between £501 and £800 the previous year.

Previously, 14% of drivers paid under £250 for their car insurance. When asked how much they pay now, only 7% said that costs were under £250. The other 7% saw costs increase, and half of those surveyed said that their premiums had risen by up to £100. A staggering 49% confirmed that while they’re currently able to afford their payments right now, any further increase would cause them to struggle financially.

Car insurance rises leave young drivers worse off

When we looked at some of the responses from different age groups, we noticed that the car insurance price hikes are actually disproportionately impacting gen-z drivers more than any other age group.

Shockingly, over a third (33%) of 18 to 24-year-olds experienced an increase of between £101 and £250 on their car insurance upon renewal, but for all other age brackets, the majority selected between £1 and £100. Nearly half (43%) of gen-z believe that there is no justification for this price increase.

Looking at how gen-z pays for their car insurance, it looks like they also choose the more expensive option. Half (50%) of 18 to 24-year-olds, the biggest of all age brackets, said that they pay for their car insurance in monthly instalments arranged by their insurer.

Gen-z are also considering drastic changes in order to save money, as 17% say they’re considering getting rid of their vehicle altogether as the cost of car insurance has become far too expensive, 26% say they’re considering downsizing their vehicle and 25% say they’ll use public transport in order to reduce their mileage.

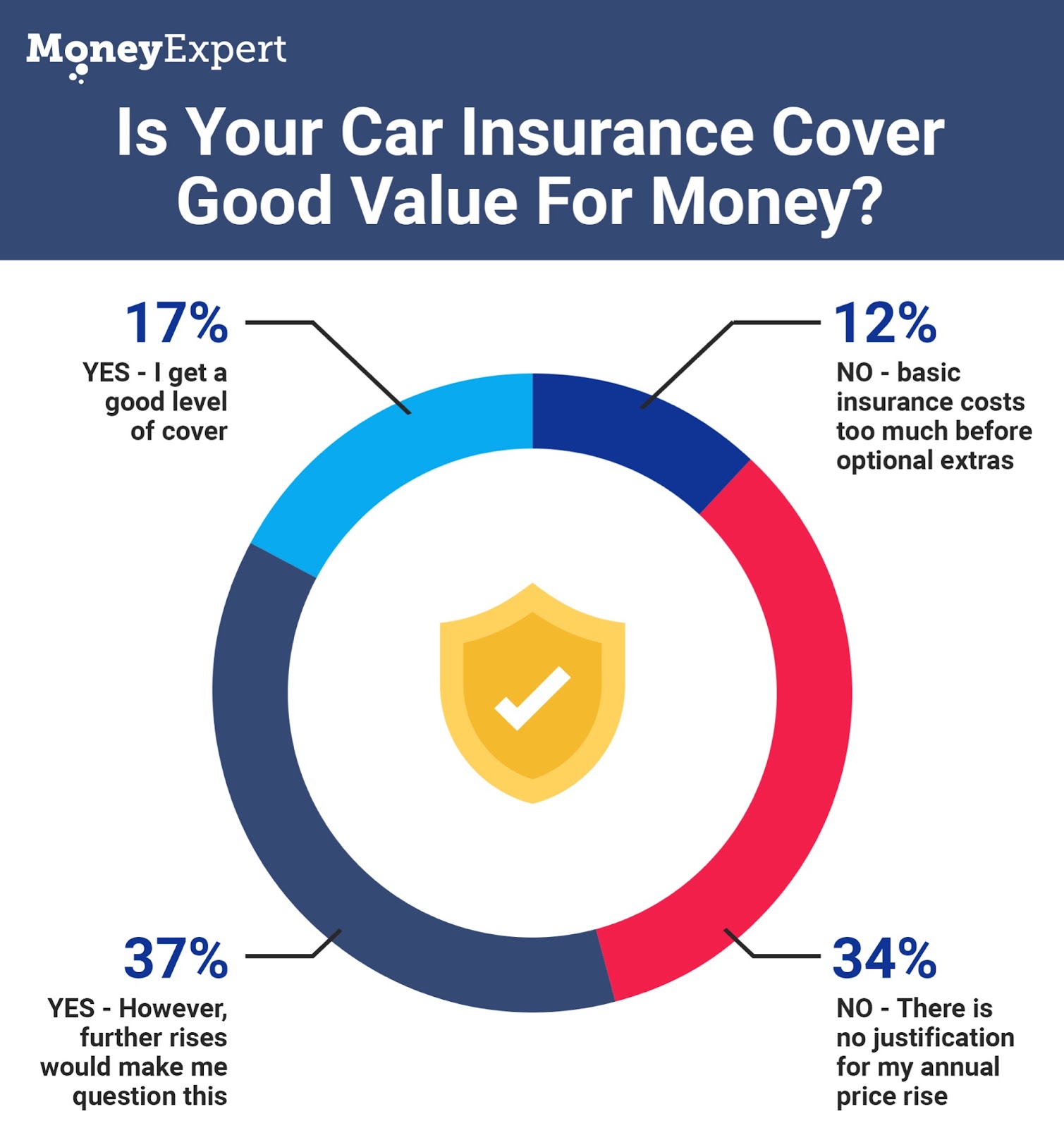

Is car insurance cover good value for money? UK drivers have their say

With costs increasing for drivers, we wanted to use the survey to find out whether they think that they get good value for money with their current car insurance provider in relation to price increases.

Almost two-fifths (37%) said that the level of cover they receive is good value for money. However, many are concerned with the rises and 34% aren’t happy and feel that there is no justification for the annual price increase.

Interestingly, nearly one-fifth (17%) explained that while they do feel like they get good value for money, a further price rise would question this.

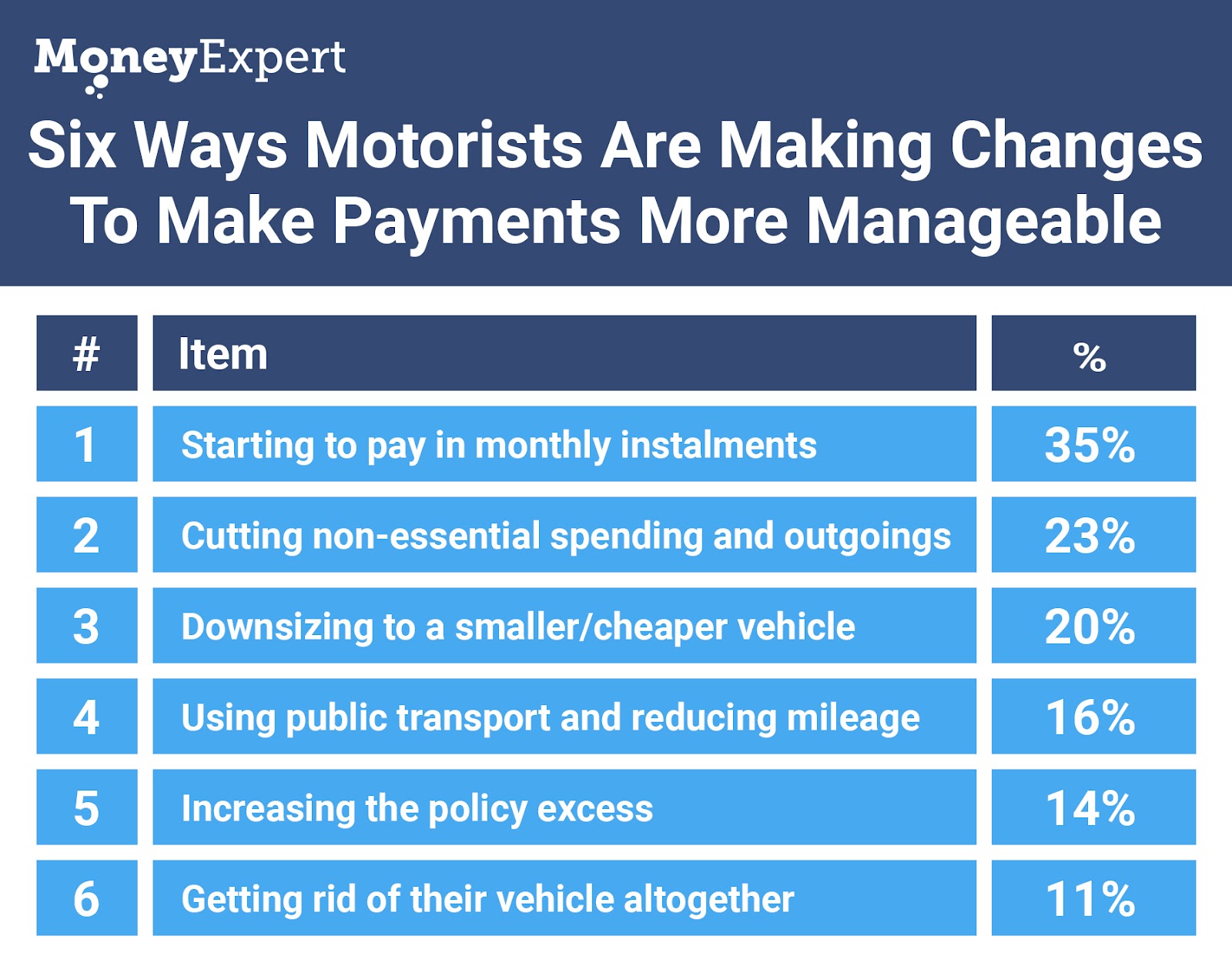

What changes will drivers make to save money?

We wanted to know whether drivers would be making any changes to save money and help them meet rising car insurance payments. With rising costs coming at homeowners from all angles, it’s no surprise motorists are looking at ways they can save money.

Over a third (35%) of respondents revealed that rising costs mean that they will switch from paying upfront to paying in monthly instalments to make their car insurance payments more manageable, despite this being the more expensive option in the long-term.

Non-essential spending will also take a hit, as nearly a quarter (23%) have said they’ll be looking at their outgoings and cutting their spending in order to afford increasing car insurance payments.

Interestingly, 20% will consider downsizing their vehicle to help reduce costs, and 16% will consider using public transport and reducing mileage to bring insurance costs down. Another 14% would consider increasing their excess to reduce the overall cost of their premium.

Shockingly, only a quarter (25%) of UK drivers say that they’re able to afford their car insurance payments, without making any changes at all.

How do drivers look for the best car insurance deals?

The survey asked how UK drivers look for the best deals when their premiums are coming to an end to find out what methods people are using to save themselves money, and whether they need more advice on the best way to go about getting the best deal for them. This is especially important at a time when costs are rising across the board.

Our findings revealed that the majority (78%) of respondents use a price comparison site to compare deals and find the best one for them.

When it comes to other ways of renewing their car insurance, 16% said that they go directly to the insurer online or over the phone to find out what their offers are, and 4% use an insurance broker.

We also wanted to know whether they stuck with the same provider or whether they moved around depending on who was offering the best deal.

Our survey results confirmed that UK motorists prefer to shop around than stay loyal to one provider, while nearly two-thirds (54%) said that they switch to different companies every year and that it depends on who provides the most competitive price.

However, over a quarter (26%) choose convenience over cost, as they take their renewal quote offer from their current provider each year to save time.

Commenting on the results, Liz Hunter, our Commercial Director said, “Motorists of all ages have seen their car insurance increase over the last few months and will be feeling the pinch from all areas when it comes to their household budgets, particularly as the cost of living crisis continues to impact households, despite inflation stabilising and lending interest rates coming down.

But perhaps unsurprisingly, our survey also identified that young adults, especially those between the ages of 18 and 24, have been disproportionately affected by rising car insurance costs.

Car insurance has always been more expensive for young and inexperienced drivers, but the stark reality is that this demographic is now grappling with increases far exceeding those faced by older age groups, with 17% of those aged between 18 and 24 considering getting rid of their vehicle altogether.

This could have long-term consequences on the mental and physical health of our young people, as being without a car can have a significant impact on employment opportunities, access to essential services and social lives, too.

This highlights the urgent need for government support and solutions to address the widening gap in accessibility and affordability of essential services for our younger demographic.”

How to reduce your car insurance premiums

Liz Hunter continues, “According to our survey, nearly a quarter of respondents will be looking to save money by reducing non-essential spending. Since having car insurance is a legal necessity, many of those who rely on having a car now need to find a way to insure their car without breaking the bank.”

“Luckily, there are a number of options that may help consumers reduce the costs and obtain a much better deal. Here is our advice on what consumers can do to get the best deal on their next insurance policy to help reduce costs:”

-

Use a price comparison site

When it comes to choosing a new policy when you’re due to renew, you should always use a price comparison site to compare rates from multiple providers to find the best deal. Not only will it save you time but it can help save up to £504* and offer a wider range of providers. For example, we can help you compare deals from over 100 of the UK’s top providers. Simply input your details and the comparison site does the rest, scouring a number of insurance companies to find the best deal for your needs. If you find one cheaper than your current provider is offering, you could always call them up first and see whether they can match it or offer you something better.

As of the 1st January 2022, car insurers were banned from charging existing policy holders more for their renewal price, compared to what they would charge for new customers. This means that existing customers will be offered the same price as new customers for their insurance renewal. These rules now mean that customers could find that the best deal is their renewal price, however, it’s still worth doing your research on comparison sites and shopping around to get the best price you can.

-

Check for unnecessary added extras

Insurers are understandably keen for you to buy as many add-ons to their policies as possible, such as lost key cover, legal cover, no claims bonus protection and windscreen cover. The question to ask yourself is, do you actually need these additional levels of cover? If you deem it unlikely that you’ll lose your keys, consider opting out for this and look at extras more worthwhile such as no claims bonus protection that may actively save you money in the long run.

-

Pay upfront rather than monthly

While 35% said that the rising costs have meant they will choose to pay for their car insurance in monthly instalments to make payments more manageable. Sometimes insurers actually charge more for this option as you’re opted into a credit agreement and paying interest on top of the annual premium.

If you can, it’s worth paying for your insurance in full to get the very best deal. If you’re unable to pay upfront, you could also consider signing up for a 0% credit card, pay your insurance in one go and then make smaller monthly payments to your credit card provider until it’s paid off instead, to avoid overpaying on your insurance.

-

Bundle your policies

Do you have other policies with any insurance providers for a pet or home, for example? If so, it might be worth calling them up and seeing whether you could save money by bundling your insurance policies with the same provider. Many insurers offer discounts for having multiple policies with them.

-

Renew in good time

Insurers will ask for a start date for your insurance when you’re conducting your search. If you need cover urgently within the next few days, you may be quoted a higher premium compared to if you had looked earlier. So if you can, try to search and buy your insurance policy two to three weeks before you need it, which should help lower the price.

-

Add whether you work from home

If you work from home and never travel to a place of work, it helps to make sure you declare this when buying your policy. Always ensure you don’t opt for ‘commuting’ when insurers ask how you will use your vehicle, and you may be able to reduce your premium due to your car being off the road during peak times.

-

Consider Black Box Insurance

Some insurance providers will offer black box insurance. A black box uses telematics to gauge how you use your car, looking at the speed, acceleration and the time and day you drive it. It’s particularly popular with new drivers as it helps reduce insurance costs significantly whilst promoting careful driving. Some policies even reward your careful driving by lowering your monthly premiums over time.

However, if the black box notices you speeding, it can also increase your premiums, so due care and attention are required if you opt for this type of insurance. You should also factor in the cost of the box and installation, as this could easily outstrip the cost of just taking an orthodox policy if you’re a low-risk driver without a history of making a claim.

-

Maintain a clean driving record

Avoid reckless driving and getting points on your licence to keep your driving record clean, as safer driving habits can lead to lower premiums. Building and protecting your no claims bonus can also help keep premiums low.

A no claims bonus is accrued and added each year you don’t make a claim on your car insurance, which proves to insurers that you’re less likely to make a claim compared with someone without a no claims bonus, all else being equal. You can opt to protect your no claims bonus after five years for an extra fee. It’s well worth considering this add-on as it prevents your insurance from increasing significantly in the event of you having to make a claim in the future.

-

Add a named driver

A named driver is an additional person that you add to your car insurance policy, that will then have permission to drive the insured vehicle. Adding a more experienced driver to your policy (such as a parent) can reduce the cost of your premium significantly, as it may reduce the overall risk in the eyes of your insurer.

It’s a popular option with high-risk or inexperienced drivers who want to reduce the overall cost of their policy, such as young adults or the very elderly. It’s not just useful for high-risk drivers though; additional driver cover can also save money for couples and families who share their car, or those who don’t drive so frequently.

For experienced drivers who want to add a high risk driver on their policy however, it can significantly increase insurance premiums, so be aware.

-

Think about your the type of your car

Something to remember is that the type, size and age of the car will have a bearing on the cost of your policy. As a general rule, cars with smaller engines and more security features will cost less to insure. So it’s worth checking the potential cost of insurance before purchasing a new or second-hand car to try and save money

*51% of consumers could save £504.24 on their Car Insurance. The saving was calculated by comparing the cheapest price found with the average of the next four cheapest prices quoted by insurance providers on Seopa Ltd’s insurance comparison website. This is based on representative cost savings from September 2023 data. The savings you could achieve are dependent on your individual circumstances and how you selected your current insurance supplier.

METHODOLOGY:

Survey Date: January 2024

Audience Participation: 1000 UK residents

Demographics: Male and Female, aged 18+

Survey Requirements:

-

Respondents must be able to drive and have a current car insurance policy

-

Respondents must have renewed their car insurance policy within the last 6 months